The Advisor's Edge - March 2026

The game is rigged. Let's talk about how to change it.

I’ve been an employee benefits advisor for 24 years. I’ve sat across the table of a lot of employers during renewal season and delivered a lot of difficult numbers.

This past January was different.

The 2026 renewal cycle was the most brutal I’ve experienced in my career. Not just because of the size of the increases — though double-digit renewals were routine across our book of business — but because of how many clients had done everything right and still got hammered.

After two decades in this industry, I’ve come to an uncomfortable conclusion: the traditional insurance market isn’t broken. It’s working exactly as designed. Just not in your favor.

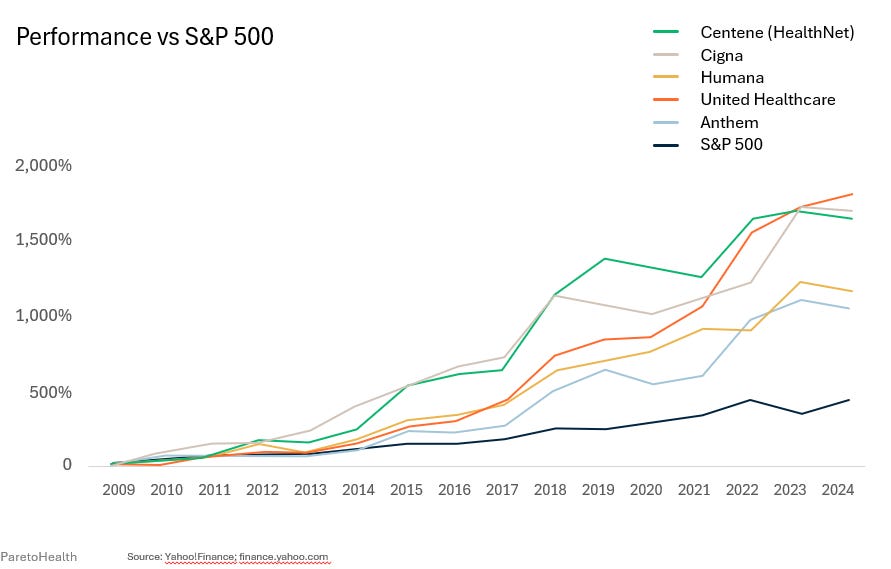

Family premiums rose 111% between 2010 and 2020. Worker earnings grew 27%. The largest health insurance carriers have dramatically outperformed the S&P 500 since the Affordable Care Act took effect. The Medical Loss Ratio — designed to limit insurer profits — actually codified them. When profit is calculated as a percentage of premium, higher claims drive higher premiums, and higher premiums drive higher profit. Low claims year? The carrier keeps the surplus. High claims year? You pay for it at renewal. The insurer wins either way.

There is a better way. Most midsize employers have never heard of it.

What Is a Health Insurance Captive?

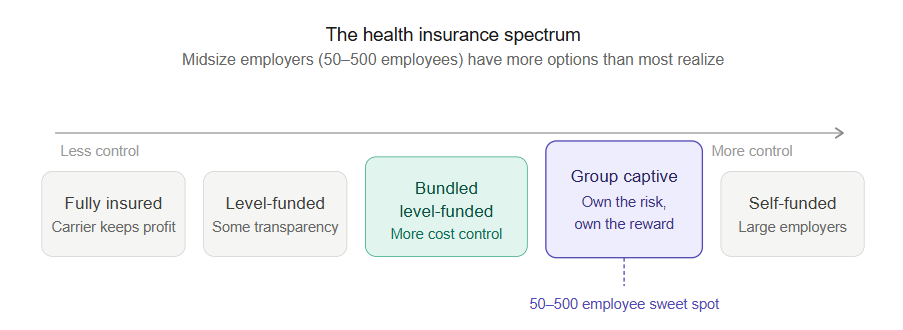

Most employers think of health insurance as binary — you’re either fully insured or you’re not. The reality is a spectrum:

Fully Insured → Level-Funded → Bundled Level-Funded → Group Captive → Self-Funded

A group captive sits in the middle of that spectrum. It’s a formalized risk-sharing arrangement among a community of like-minded, well-managed employers. Instead of paying premium to a carrier and never seeing it again, member employers pool their risk — and when the pool performs well, the financial benefit flows back to the members. In most captives, you don’t just share in the pool’s performance. You become an owner in the captive organization itself.

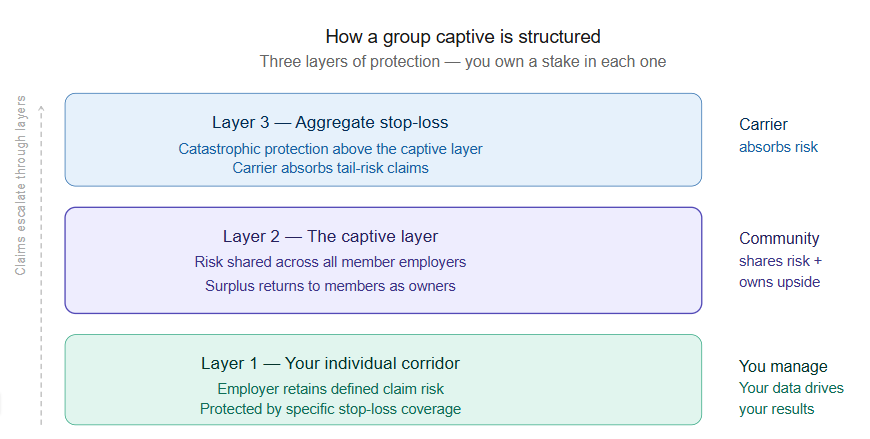

The funding structure has three layers. Your individual corridor, where you retain a defined level of risk protected by specific stop-loss coverage. The captive layer, where claims above your corridor flow into the shared community pool. And aggregate stop-loss coverage above the captive layer for catastrophic protection. When the captive layer performs well, the surplus belongs to the members — not to a carrier’s shareholders.

That’s a fundamentally different financial relationship than traditional insurance.

Three Questions to Evaluate Any Captive

Not all captives are created equal. Before any employer considers one, three questions should drive the evaluation.

1. How large is the membership? Risk-sharing only works when there’s enough risk to share. A captive with a handful of members concentrates exposure. What you’re looking for is scale — thousands of employers, hundreds of thousands of covered lives. Think of it like a mutual fund: a portfolio with five stocks isn’t diversified.

2. What stop-loss terms protect members when large claims hit? The frequency of catastrophic claims exceeding $2 million has increased 14.5 times for midsize businesses over the past three years. Under traditional insurance, a large claim triggers a laser at renewal — a higher individual deductible assigned to that specific claimant, plus a premium increase. You get hit twice. Look for captives offering rate caps, guaranteed no-new-laser protections, and multi-year rate stability.

3. Does the captive demand cost containment across all members? This is the question most employers never think to ask — and the most important one. A captive that allows members to opt in or out of cost containment is only as strong as its least-engaged members. The best captives require participation in vetted cost containment programs across the entire membership. When every employer in the pool is actively managing utilization, the whole community benefits. Your neighbors’ health management directly protects your renewal.

Is Your Organization a Candidate?

Strong captive candidates generally share a few characteristics: relatively clean claims history, a stable workforce, genuine investment in employee wellbeing, and leadership willing to think in years rather than months. As explored in The Wellness Abandonment Tax, healthy populations cost less — and that’s not just a wellness talking point, it’s the actuarial basis for captive participation.

The ideal window to begin the conversation is 9 to 12 months before your renewal date. A feasibility analysis requires three years of claims data, a current employee census, and your existing stop-loss terms.

The employers who will win the next five years of renewal cycles aren’t the ones who negotiated hardest at renewal time. They’re the ones who changed the game entirely.

If you’d like to explore whether a captive is the right fit for your organization, reach out directly. A feasibility conversation is the logical first step — and it starts simply.

News You Can Use

1. RPW Webinar: Navigating Medicare: Financial Planning for your Health & Wealth

Medicare decisions are more than just healthcare choices—they’re strategic financial decisions that impact your retirement income, tax planning and long-term wealth preservation. Whether you’re years away from Medicare eligibility or approaching enrollment, understanding how Medicare integrates into your comprehensive financial and estate plan is essential for protecting your assets and ensuring a secure retirement.

In this session, you will learn:

The basics of Medicare, including key enrollment timelines, coverage options,

and strategic decisions that affect your financial outcomes

How to integrate Medicare planning into your overall wealth management strategy and retirement income plan

Special considerations for high-net-worth individuals, including IRMAA surcharges, tax implications, and advanced planning strategies

Register for our webinar on March 31st at 12:00 PM CT

2. Webinar replay: 2026 Compliance & Benefits Update

The benefits and regulatory environment has never been more complex. In this webinar, HUB compliance experts break down the most important developments shaping 2026 — from AI and GLP-1 cost pressures to pharmacy trends, tariffs, and new legislation like the One Big, Beautiful Bill Act — and what employers should be doing now to stay compliant, competitive and proactive.

3. Your Pharmacy Rebate Check Is About to Get Smaller

If your plan has historically relied on pharmacy rebates to offset costs, 2026 is the year that math starts to change — and not in your favor.

HUB’s Pharmacy Consulting Practice has released a client briefing on expected changes to pharmacy rebate yield, and the headline is straightforward: rebate checks received in 2026 and 2027 will likely come in below historical levels and possibly below what your PBM projected.

Three forces are converging. First, the Inflation Reduction Act’s Maximum Fair Prices took effect January 1, 2026, covering ten high-cost drugs including Eliquis, Jardiance, Farxiga, and Stelara. Several have already seen list price reductions of 37–75% — and since rebates are typically calculated as a percentage of list price, lower list prices mean lower rebates. Second, accelerating biosimilar adoption for Humira and Stelara is shifting utilization away from the high-rebate brand products that have anchored PBM underwriting for years. Third, direct-to-consumer pricing programs — including Lilly Direct, Novo Care, and the recently launched TrumpRx program — are adding downward pressure across a broader range of products.

One thing worth watching closely: PBMs are increasingly applying “rebate credits” — the calculated difference between brand and biosimilar costs — in ways that lack transparency. If you’re not sure how your PBM agreement handles this, now is a good time to review.

The shift isn’t all bad news. Lower list prices and biosimilar adoption can reduce your members’ out-of-pocket costs. But the net impact on your plan will depend on your specific utilization of affected products and how your PBM contract is structured.

If you’d like to discuss how these changes may affect your plan specifically, reach out and we can walk through it together.

Worth Sharing

A couple of months ago, I sat down with a representative of University of Colorado Health System (UC Health). During our lunch, she shared that UC Health would be building (yet) another hospital in the Broomfield area.

If you’ve been paying attention along the front range, UC Health has built a lot of hospitals over the past 10 year. I point blank asked her why, and suggested that their continual expansion was a contributor to our cost crisis.

She responded by saying “We need the capacity. Our hospitals are full.”

If true, that’s very disappointing. It’s a leading indicator of how poor our collective health has become.

A week ago, my dad, who is partially paralyzed after a stroke in 2019, took a fall. Bleeding profusely and unable to get himself off the ground, he was taken to the ER at the Medical Center of the Rockies (MCR) by ambulance.

Ultimately, they decided to admit him for further observation. As it would turn out, the hospital was full. We had to wait at the ER until the ambulance activity decreased and a unit could be made available to transfer him to Poudre Valley Hospital in Fort Collins.

The hospital was full. Let that sink in. The UC Health rep was speaking truth.

We have a problem that goes beyond premium management. We have a people problem.

I’m working on an in-person event in late May or early June for us to tackle this problem head on. Stay tuned for more details.

I’m also working with a couple of vendor partners to create an affordable program that helps people create insights into their personal health before they need a hospital bed. I hope to roll out additional detail on that soon, also.

In the meantime, if you’d like to have a conversation about some ways we can mutually build a better, more proactive health and performance program, please reach out.

I recently heard a saying, “Bigger isn’t better. Better is better.”

We, collectively, have to do better.

Thank you for reading.

Jim Sampson Employee Benefits Advisor | HUB International theebadvisor.com