The Game Is Rigged. Here's How to Change It

What midsize employers need to know about health insurance captives — and why the traditional model was never designed to work in your favor.

Throughout the 24 years that I’ve been advising on employee benefits, I’ve sat across the table from hundreds of employers during renewal season, delivered difficult numbers, and helped navigate some genuinely tough conversations.

This past January was different.

The 2026 renewal cycle was the most brutal I’ve experienced in my career. Not just because of the size of the increases — though double-digit renewals were routine across our book of business — but because of how many clients had done everything right and still got hammered. They’d managed their populations. They’d invested in wellness. They’d tightened their plan designs. And still, the increase came.

Much of this has been driven by our own collective lifestyle decisions. It doesn’t take robust investigative skills to quickly discern that we, as a collective society, are not in great shape.

But that doesn’t fully account for the mess we just experienced. I found myself asking a question I ask every difficult renewal season, but with more urgency this time: why are we still playing a game that was never designed for us to win?

The answer, as I’ve come to understand it over two decades in this industry, is structural. The traditional insurance market isn’t broken. It’s working exactly as designed — just not in your favor.

There is a better way. It’s been available to midsize employers for years. Most have never heard of it. And the advisors who should be recommending it often don’t, for reasons we’ll get to.

It’s called a health insurance captive. And if you’re a midsize employer between 50 and 500 employees, this may be the most important conversation you’re not having.

The Math Doesn’t Lie

Let’s start with some uncomfortable arithmetic.

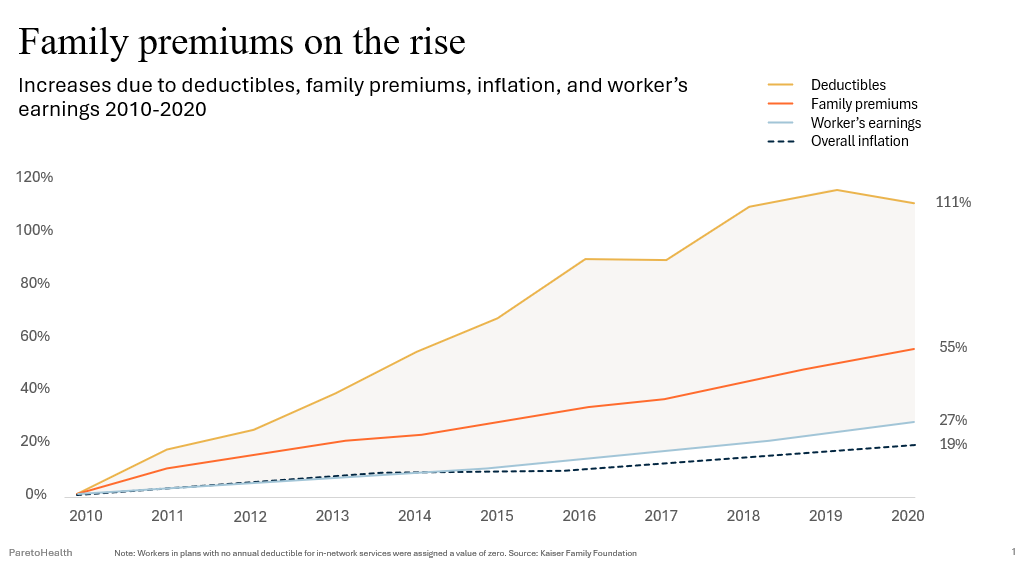

Between 2010 and 2020, family health insurance premiums increased 111%. Worker earnings grew 27%. Overall inflation rose 19%. Deductibles climbed even faster than premiums — up 111% in the same period, according to the Kaiser Family Foundation.

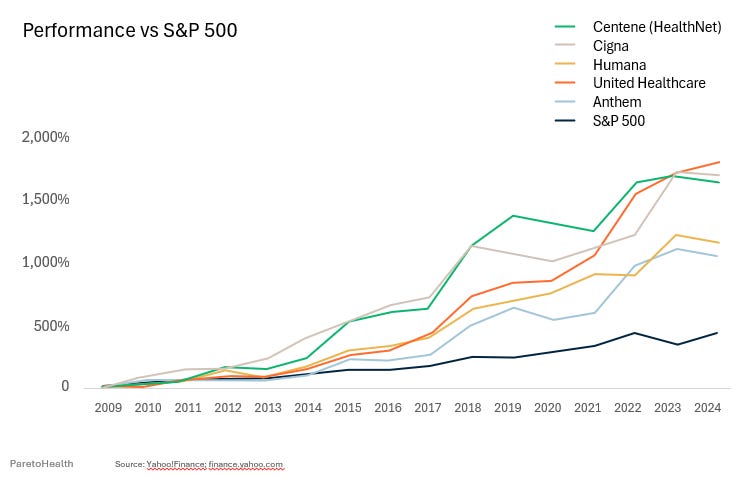

Meanwhile, the stock prices of America’s largest health insurance carriers — what the industry calls the BUCAs — have dramatically outperformed the S&P 500 since the Affordable Care Act took effect.

Think about that for a moment. The law designed to make healthcare more affordable has coincided with an era of extraordinary profitability for the carriers managing your plan.

This isn’t an accident. It’s the Medical Loss Ratio at work.

The ACA capped insurer profits by requiring that a minimum percentage of premium revenue go toward actual claims — 80% for small groups, 85% for large groups. The intent was to limit excess profit. The reality was something different.

When your profit is calculated as a percentage of premium, the equation becomes simple: higher claims drive higher premiums, and higher premiums drive higher profit. The MLR didn’t eliminate the incentive to let costs rise. It codified it.

The result? Carriers with the resources and data to engineer a different cost trajectory have little financial incentive to do so. As we explored in Healthcare Cost Drivers Secretly Killing Your Success, this structural conflict is one of the most underappreciated forces driving your renewal — and it’s hiding in plain sight.

Low claims year? The carrier keeps the surplus. High claims year? You pay for it at renewal.

The insurer profits either way. You don’t.

BUCA Stock Prices Since the Passage of the ACA

There Is a Spectrum

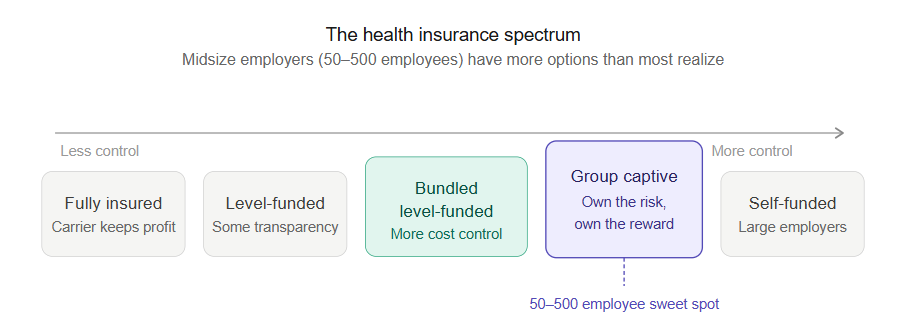

Most employers think of health insurance as a binary choice: you’re either fully insured or you’re not. That’s not accurate — and that misunderstanding is costing midsize employers real money.

The reality is a spectrum:

Fully Insured → Level-Funded → Bundled Level-Funded → Group Captive → Self-Funded

Each step along that spectrum represents more transparency, more control, and more opportunity to benefit when your workforce is well-managed. Each step also requires more engagement, more data, and more financial participation.

Most employers in the 50 to 500 employee range are stuck at the left end of that spectrum — fully insured — even when their claims experience, workforce stability, and financial position would make them strong candidates for something further right.

A group captive sits in the middle of that spectrum. It gives you the transparency and data access that comes with more control over your plan, combined with the risk protection of a shared community. It’s not a leap off a cliff. It’s a deliberate step toward a structure that rewards you for managing your population well.

How a Group Captive Actually Works

A group captive is a formalized risk-sharing arrangement among a community of like-minded, well-managed employers. Instead of paying premium to a carrier and never seeing it again, member employers pool their risk together — and when the pool performs well, the financial benefit flows back to the members.

In most captives, this goes one meaningful step further: you don’t just share in the pool’s performance. You become an owner in the captive organization itself. That ownership stake changes the entire relationship. You have a seat at the table, a voice in how the captive is managed, and a direct financial interest in the health of every other member organization.

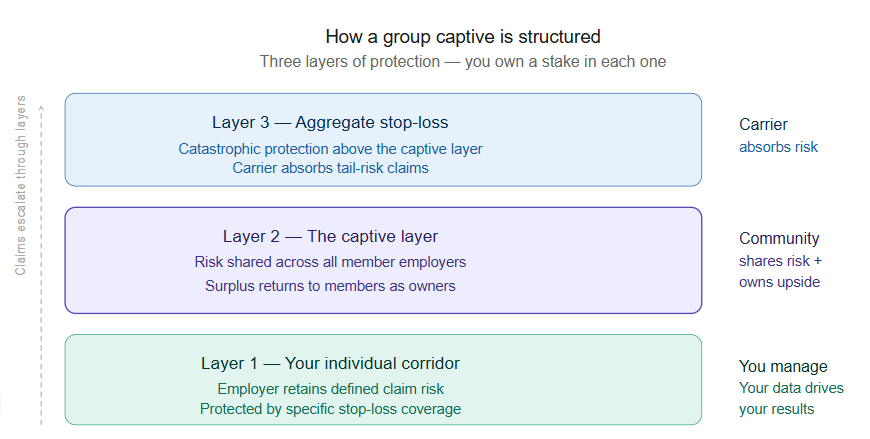

The funding structure has three layers:

Layer 1 — Your Individual Corridor Each employer retains a defined level of individual claim risk, protected by specific stop-loss coverage. Claims below this threshold are your responsibility. This is where your own data and population health management has the most direct financial impact.

Layer 2 — The Captive Layer Claims above your individual threshold, up to a defined ceiling, flow into the captive. This is the shared risk layer — where the community absorbs the volatility that would otherwise devastate a single employer. A bad year for one member is buffered by the good years of many others.

Layer 3 — Aggregate Stop-Loss Catastrophic exposure above the captive layer is covered by aggregate stop-loss insurance. This is your protection against the tail risk — the claims no employer can predict or absorb alone.

When the captive layer performs well — meaning total claims come in below the pooled funding — the surplus belongs to the members. Not to a carrier’s shareholders. To you, as an owner.

That’s a fundamentally different financial relationship than traditional insurance.

Why Catastrophic Claims Change Everything

Here is a data point that should stop you cold.

The frequency of catastrophic claims exceeding $2 million has increased 14.5 times for midsize businesses over the past three years alone, according to the HCC Annual Report 2024.

To put that in context: gene therapy now runs approximately $3 million per intervention. Advanced cancer treatment can reach $1 million. Organ transplants approach $750,000. Dialysis runs $600,000 annually.

These are no longer rare edge cases. They are increasingly routine events — and a single one can reshape your entire cost trajectory for years.

Here’s why that matters so much under traditional insurance: when a high-cost claimant surfaces in your plan, the carrier responds at renewal with two potential punishments. First, they will increase your premium based on your experience. Second, they (depending on your funding scenario) could apply what’s called a laser, a higher individual deductible assigned specifically to that claimant, meaning you absorb more of their costs in the next plan year. You get hit twice.

Under a well-structured group captive, that dynamic changes. The catastrophic risk is absorbed by the community, protected by stop-loss terms that don’t allow the carrier to laser your worst claimant year after year. The cost curve flattens. The double hit disappears.

As we discussed in the December 2025 edition of The Advisor’s Edge, catastrophic claims are no longer a planning edge case. They belong at the center of your benefits strategy.

Three Questions to Evaluate Any Captive

Not all captives are created equal. The structure matters less than the community you’re joining and the terms protecting that community. Before any employer considers a captive, three questions should drive the evaluation.

1. How large is the membership?

Risk-sharing only works when there’s enough risk to share. A captive with a handful of members concentrates exposure — one bad year for two or three employers can destabilize the entire pool.

What you’re looking for is scale. Thousands of employers, not dozens. Hundreds of thousands of covered lives, not tens or hundreds. That level of scale creates the actuarial cushion that enables year-over-year predictability, and it delivers negotiating leverage that no individual midsize employer can replicate on its own.

Think of it like a mutual fund. A portfolio with five stocks isn’t diversified. A portfolio with thousands of positions weathers volatility differently. The same principle applies to the pool of employers sharing your captive’s risk.

2. What stop-loss terms protect members when large claims hit?

This is where the fine print separates good captives from great ones.

Look for three specific protections: a cap on annual rate increases, guaranteed protection against new lasers for existing members, and multi-year rate stability that doesn’t evaporate after a single large claim.

Without these protections, you’ve traded one volatile structure for another. With them, you gain the ability to plan — not just for the current year, but for the three to five years ahead.

Employers who evaluate captives based on year-one pricing alone are making the same mistake they make in traditional insurance. The real value is in the trajectory, not the starting point. Captive members who commit to the structure and work the program consistently report savings that compound meaningfully over time.

3. Does the captive demand cost containment across all members — or is it every employer for themselves?

This is the question most employers never think to ask. It is also the most important one.

A captive that allows members to opt in or out of cost containment strategies is only as strong as its least-engaged members. If your neighbors in the pool are mismanaging their populations — high-cost claimants going unmanaged, behavioral health issues unaddressed, pharmacy spend unchecked — you share in the consequences even if your own population is well-run.

The best captives address this by requiring participation in vetted cost-containment programs across the entire membership. Not as a suggestion. As a condition of membership.

When every employer in the pool actively manages utilization, controls pharmacy spend, addresses behavioral health early, and invests in workforce wellbeing, the whole community benefits. Your population’s health management protects your renewal. So does everyone else’s.

This is the flywheel that traditional insurance structurally cannot offer. As we explored in The Silent Claims Accelerant, behavioral health conditions alone account for 56.5% of total plan costs for the individuals carrying those diagnoses. That is a community problem. A well-run captive treats it as one.

This Problem Is Bigger Than Your Budget

Before we discuss whether a captive might be right for your organization, it’s worth stepping back from the spreadsheet for a moment.

Healthcare costs are not just a CFO problem. They are a workforce problem.

According to the Allstate Health Solutions Benefit Survey, 62% of employees at midsize employers believe their healthcare contributions are too high. Healthcare is the leading cause of personal bankruptcy in America. And 78% of employees say they would leave their current employer for better benefits.

The renewal shock you just survived is not abstract to your workforce. Every time you raise deductibles, increase employee contributions, or narrow the network to control costs, it lands personally on the people doing the work. It affects their financial security, their decisions about seeking care, and ultimately their decision about whether to stay.

The employers winning the benefits conversation — in both cost and talent — are the ones who’ve stopped treating health insurance as an annual line item and started treating it as a long-term strategic investment.

That shift in thinking is exactly what a well-designed captive makes possible.

Is Your Organization a Candidate?

A group captive is not the right fit for every employer. But many more midsize employers qualify than realize it. Here is what the profile of a strong captive candidate looks like.

Your claims history is relatively clean. You don’t need a perfect record — a few difficult years won’t automatically disqualify you — but underwriters are looking for employers who demonstrate intention around population health management. Three years of claims data is the starting point for any serious feasibility conversation.

Your workforce is reasonably stable. High turnover creates unpredictability in population health data, which makes it harder to price risk accurately. Employers with stable, engaged workforces are the foundation of every strong captive.

You’re already investing in employee wellbeing — or you’re ready to. As explored in The Wellness Abandonment Tax, healthy populations cost less. That’s not just a wellness talking point — it’s the actuarial basis for captive participation. Employers who proactively manage their workforce’s health bring better risk to the pool, and that translates directly to financial performance.

Your leadership is ready to think in years, not months. The fully insured model conditions employers to think in 12-month increments. Captive participation rewards a longer view. The financial benefits compound over time — employers who commit to the structure and manage their population consistently see meaningful savings grow year over year.

Your financial position supports participation. Captives require more upfront financial engagement than fully insured plans. The tradeoff is access to surplus dollars when you perform well. If cash flow is a primary constraint, a feasibility conversation will help clarify whether the timing is right.

The ideal window to begin that conversation is 9 to 12 months before your renewal date. A feasibility analysis typically requires three years of claims data, a current employee census, and your existing stop-loss terms. The process is not burdensome — but it does require intention.

What to Ask Your Advisor

Here is an honest observation after 24 years in this business: not every advisor is equipped to have this conversation.

Placing a group in a captive requires a different skill set than renewing a fully insured plan. It requires relationships with captive managers, familiarity with stop-loss markets, and the analytical capability to evaluate whether a specific captive’s structure, membership, and terms actually deliver what they promise.

Complacent advisors don’t recommend captives. Not because they aren’t right for their clients — but because the work is harder, the learning curve is steeper, and the path of least resistance is to renew what’s already in place. We addressed this pattern directly in Healthcare Cost Drivers Secretly Killing Your Success — broker complacency is one of the most expensive forces in your benefits program, and most employers never see it.

If your advisor has never placed a group in a captive, it doesn’t automatically disqualify them. But it should prompt a direct conversation about whether they have the relationships and expertise to guide you through the process — or whether a second opinion is warranted.

The right advisor asks the three questions above before recommending any captive. They evaluate pool size, stop-loss terms, and cost containment requirements with the same rigor they’d apply to any plan design decision. And they’re transparent about their own experience and limitations.

The Game Can Change

The traditional insurance market is not going to fix itself. The incentives running the system benefit carriers, not employers. Premium revenue is the engine. Your cost increases are the fuel.

But midsize employers in the 50 to 500 employee range are not without options. They are not too small to demand transparency. They are not too small to share risk intelligently. They are not too small to benefit when their workforce is healthy and their population is well-managed.

A group captive is not a silver bullet. It is a structure that rewards employers who are willing to engage — with their data, with their population, with their long-term strategy.

The employers who will win the next five years of renewal cycles are not the ones who negotiated hardest at renewal time. They are the ones who changed the game entirely.

You have more control than you think. The question is whether you’re ready to use it.

If you’d like to explore whether a captive is the right fit for your organization, I’d welcome the conversation. A feasibility analysis is a logical first step — and it starts simply. Reach out to me directly at jim.sampson@hubinternational.com and let’s find out together.

Sources:

Kaiser Family Foundation, Employer Health Benefits Survey 2020

HCC Annual Report 2024

Allstate Health Solutions Benefit Survey 2024

Milliman (independent review of captive member savings data)